Dealing with the Aftermath of a Home Fire

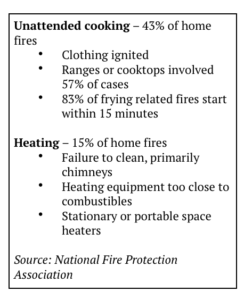

Each year in the United States there are over 360,000 home fires reported to fire departments. The chance of your household becoming part of these statistics in your lifetime is 1 in 4. If you include fires not reported to the fire department, estimates from the National Fire Prevention Association indicate that each household can expect a fire once every 15 years, or five times in a lifetime. 43% of these fires start in the kitchen, 15% involve heating equipment and the remainder involve electrical, smoking, clothes dryers, lightning, candles and children playing with fire. Regardless of the origin, home fires are a realistic risk that needs to be planned for. One of the reasons we carry fire insurance and may be required to do so to secure mortgage financing.

Most home fires do not involve total losses. According to a study done by the Insurance Information Institute (2004-2008), the average claim for home fires was $25,375. Unfortunately, what is left after almost every home fire is damage from flames, heat, smoke and water. Fire departments may also cut holes in walls to search for hidden flames and holes in the roof to vent the heat.

Most home fires do not involve total losses. According to a study done by the Insurance Information Institute (2004-2008), the average claim for home fires was $25,375. Unfortunately, what is left after almost every home fire is damage from flames, heat, smoke and water. Fire departments may also cut holes in walls to search for hidden flames and holes in the roof to vent the heat.

Smoke Damage can be cleaned, but needs to be done as soon as possible, primarily due to the effects of ash residue, which is acidic. The longer it takes to remove smoke, the more damage it causes. Plastics are permanently discolored within minutes, fiberglass and appliance finishes within hours, clothing, upholstery and walls within a few days. If restoration does not occur wit

hin a few weeks, costs skyrocket. Metals may need to be replaced, glass can be permanently etched and there is a good chance that carpeting will be permanently discolored.

Standing water and water soaked materials need to be quickly dried to prevent permanent loss, formulation of mold or odors that are difficult to remove.

FEMA, in its publication “After the Fire – Returning to Normal”, provides advice on how to respond, resources that are available to help and the process for handling the damage done. Some key considerations:

- Before a fire occurs, make sure you understand what your homeowner insurance covers. Have a plan for emergency situations that includes access to important contact information and insurance policies, and resources to provide short term food and shelter for the family.

- If you and your family need immediate assistance with food and shelter, there are a number of relief agencies to provide assistance

- Contact your insurance company as soon as possible. They can arrange for helping with immediate needs, assign someone to assess the damage, and get the process moving to begin clean-up and restoration.

- A professional restoration service will likely be recommended, and is worth the investment. These services provide the best option for saving water and smoke damaged materials and restoring things to as normal as possible.

- Contractors may need to be ordered to repair damage caused during the fire response process.

For additional information, visit:

International Institute or Inspection, Cleaning and Restoration – www.iicrc.org

National Fire Protection Association – www.nfpa.org

FEMA “After the Fire, Returning to Normal” – www.usfa.fema.gov/downloads/pdf/publications/fa_46.pdf

If you are a Pharmacists Mutual policyholder, and have specific questions about your insurance coverages, please contact us at www.phmic.com.

Michael L. Warren | ARM, OHST | Risk Manager